Phillips was

one of those New Zealand economists with a lot of initials (A.B.H. aka A.W.H., aka Bill, aka William) before his

last name who got famous by noting that there appeared to be a relationship

between Ozzie and Harriett – no just kidding – between Ricky and Lucy – just kidding

again – between the unemployment rate and wage changes.

This seems

innocuous enough, but then real American economists decided to make Phillips

even more famous by making the Phillips Curve the truly greatest thing ever in

macroeconomics and skateboarding. The first thing they did was replace the wage variable with

prices. Thus, they pondered a relationship between the unemployment rate and

inflation (the percentage change in prices). I don’t think they got permission

from Phillips to make this change but that’s all history now.

Next they

gave the relationship a theoretical foundation. Fancy words – theoretical foundation.

The truth is that a monkey with the latest iPhone could have dug up this theory.

But sometimes simple things catch on. And they catch on when they support the

latest trend in macroeconomics. Recognizing that I am a bit north of my 70th

birthday, please understand that when I talk about the latest trends, I am usually

referring to the 1960s.

Unlike pink

poodle skirts and flat-tops, macroeconomic trends stay around a while. My

point today is that the Phillips Curve comes and goes in popularity, but

as I was reading the Bible – err I mean the Wall Street Journal – this week it

occurred to me that the Phillips Curve had risen from the dead again.

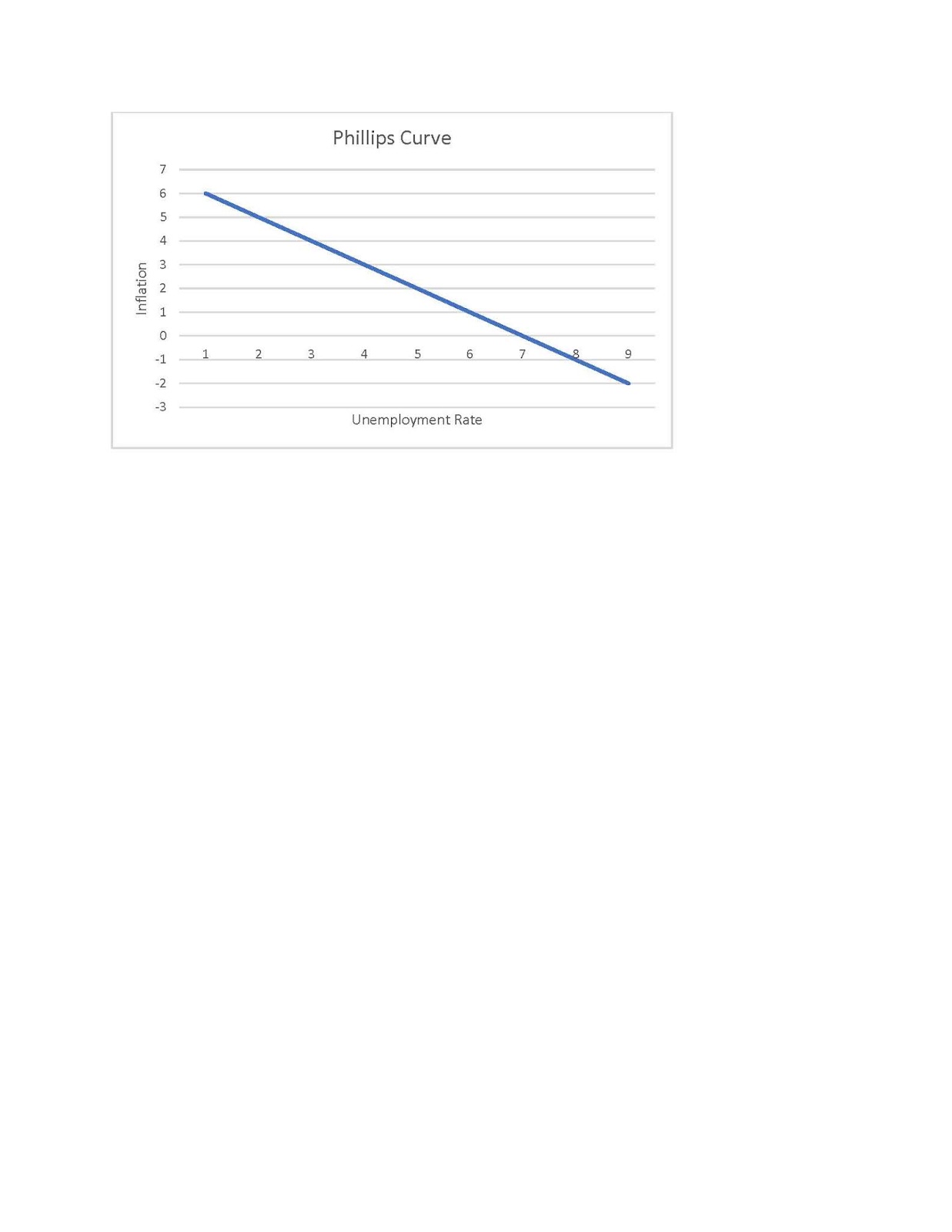

Before I get

into those juicy headlines, let’s at least review the basics of the Phillips

Curve. Below is a Phillips Curve diagram. The most popular aspect of it is the

negative slope that reveals the inverse relationship between inflation and

unemployment. Or in more common language, when one of them goes up the other one

of them goes down. Sort of like a seesaw.

One might

ponder further and say something like, “why?” Why is there a seesaw

relationship? The answer comes from short-run macroeconomics and the part of it we

call aggregate demand (AD). When households or firms or movie actors decide to

buy more stuff, firms get very happy and respond by producing and selling more stuff. To produce more stuff they need more workers and so the unemployment rate goes down. As

they hunt for more workers, they raise wages and then they must pass some or all

of that wage increase on to their prices.

Thus when AD increases – unemployment

goes down and inflation goes up. Or when AD decreases – unemployment goes up

and inflation goes down. Are you seasick from the seesaw yet? That’s basically

it. Stay awake Fuzzy.

The big deal

is that this little bit of theory is what is behind our love of using monetary

and fiscal policy to rev up spending in a flagging economy. Monetary and fiscal policies

are designed to pump up AD and therefore save the world from high unemployment –

though at a cost of higher inflation.

To get these

results, the Phillips Curve is not allowed to move around. It must sit still.

Stay Phillips Curve. Stay. Good Phillips Curve. When the Phillips Curve does

start to mosey around on the diagram, it messes up the nice seesaw and it ruins the

simple world of monetary and fiscal policy. So when the Phillips Curve is

jumping to and fro, we forget it exists. But when it sits nicely we take it for a walk.

The last 10

years or so, most economists would rather talk about soccer than Phillips

Curves. The unemployment rates around the world went down – but the inflation

rate just sat there like a squirrel on Zoloft. That is a sad story for the

Phillips Curve. Bad Phillips Curve.

But all that

is changing now. Take Turkey for example. I was going to use Ham instead but we

are actually talking about the country, Turkey. The central bank of Turkey recently decided to raise interest rates. And the government got steamed. Why was the government so mad? Because they believe that the rise in interest rates will reduce borrowing

for spending and that will cause firms to produce less and fire a lot of

workers. Of course, the country would benefit by a slide down the Phillips

Curve to lower inflation rates. But the possibility of the higher unemployment

rate was too much to risk. Clearly the government of Turkey believes in the

Phillips Curve.

Japan is

another example of the reincarnation of Phillips. Japan has been bathing in

zero or negative inflation for decades. It now seems that inflation is making a

comeback – a humble comeback but a comeback nevertheless. So should they be

concerned with rising inflation and pull back on stimulus? And risk a rise in

the unemployment rate? It's all about Phillips. A decision to curtail inflation will

cause higher unemployment if you believe in the stationary seesaw.

It goes

without saying that the same discussion is happening in the USA. The Fed has

been moving interest rates upward for more than a year now and they plan to

keep raising them in 2018 and 2019. A return to normal interest rates, like a

return to normal temperatures after sitting in a beer refrigerator for hours, makes sense. But that bit of logic is trampled by the Phillips Curve. The curve

was missing in action for 10 years but now all of a sudden it is more popular

than a soju in Insadong. Surely if the Fed

raises rates a couple more notches, the unemployment rate will rise. Surely if

the Fed worries about inflation rising, unemployment will rise.

Okay. Enough

about Phillips Curves. Next week I discuss the Davidson Curve. Just kidding again. Who moved my JD?